Fees in Asset Management Industry

The asset management industry has often been criticized for it creativity and innovation in assessing a variety of fees for the investment service provided. In an attempt to simplify the various fees for investors, we provide here an overview of the charges usually levied by different types of asset managers.

Asset management includes elements of financial statement analysis, asset selection, asset allocation, investment plan implementation, as well as ongoing monitoring of investments. These elements are performed in order to meet the required investment objectives of the investors.

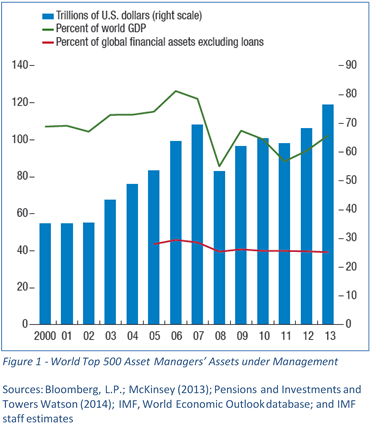

Worldwide, the asset management industry intermediates substantial amounts of money in the financial system. According to the International Monetary Fund (IMF) the total assets managed by the top 500 asset managers has doubled from 2000 to 2013. In addition, according to the IMF, “the growth of investment funds has been particularly pronounced among advanced economies during the past decade.”

According to IMF, “plain-vanilla products and privately offered separate account services dominate the markets as measured by assets under management.” Moreover, the report shows that open-end funds, exchange-traded funds, and private equity funds have shown significant growth since the global financial crisis in 2008.

Asset Management fees

In the process of managing money for their clients, asset management firms incur various types of fixed and variable fees and expenses. Fixed expenses can include payroll, office expenses, and investment research and trading equipment (ex: Bloomberg terminals). Variable expenses often include trading commission fees and soft-dollars expenses. In addition, a portion of the asset management expenses covers marketing and sales fees such as investment roadshows and client conferences that are used to present firm’s strategies, update on investment as well as meet new potential clients.

Fee Structures

There are three most common types of fees:

1. Management Fees

Management fees are charged by the asset management firm for professionally managing the money on behalf of their investors. Management fees are charge to cover firm’s fixed expenses and other administrative expenses. Typically management fee are charged as a percentage of assets under management.

2. Transaction fees

Transaction fees are incurred when investment manager trades securities and/or assets. In addition to the trading commission fees, investment manager is also subject to pay for subscription and redemption fees, brokerage fees, clearing and settlement fees.

The basic transaction fees are listed below:

- Subscription fees, also called front load fees, are charged at the time when shares or units of an asset or fund are bought. These fees are usually calculated as a percentage of the amount of the capital being invested. Some asset classes do not carry a subscription fee.

- Redemption fees, also called back load fees, are charged at the time when shares or units of an asset class or fund are sold. These fees can be calculated as a percentage of the total redemption amount or as a fixed rate per redemption transaction. Some asset classes do not carry a redemption fee.

- Brokerage fees are charged by the broker for facilitating the transactions between buyers and sellers. These fees can be fixed, variable (percentage of the transaction) or a mix of both fixed and variable.

- Trade transaction fees are associated with buy and sell transactions of securities in the secondary market. These fees are usually charged by the exchange through which the transaction was executed.

- Clearing and settlement fees, like trade transaction fees, are also usually associated with the purchase or sale of securities. These are charged by the clearing and settlement agencies through which the trade transactions flow.

- Bank transaction fees are charged by banks for transactions that are associated with cash transfers, or movement of funds from the investors to the asset manager or vice versa.

Different asset classes have specific sets of transaction fees.

3. Performance fees

Performance fees are payments made to the manager for generating a positive return. These fees align the interests of fund managers with the interests of the investors. Performance fees are calculated based on the return on the investment that the portfolio manager was able to earn during a given time period. Performance fees can be paid when the returns of the fund or portfolio exceeds a specific benchmark or a given index for the asset class.

Asset Classes

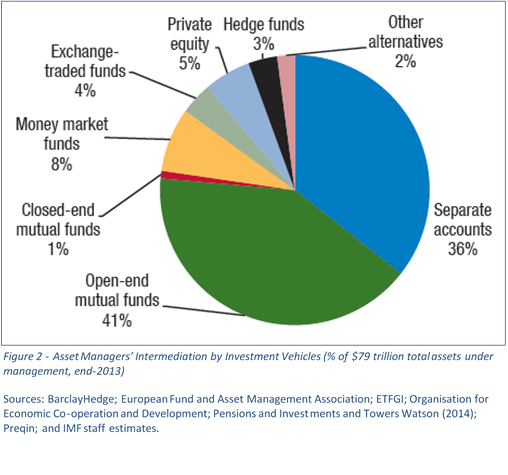

The following chart presents a breakdown of the various investment vehicles utilized by investors. It includes the investment of 43 trillion USD worldwide.

Mutual Funds

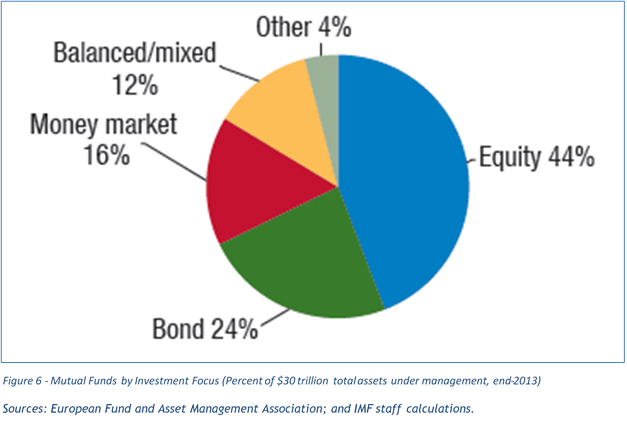

A mutual fund is made up of a pool of funds collected from many investors with similar investment objectives and risk/return profiles. Most funds invest in a combination of stocks, bonds and money market instruments. However, depending on the fund’s objective, the fund can only invest in one specific type of security (ex: equities). The graph below shows the the breakdown of mutual fund’s structure.

In addition, mutual funds can diversify their investment by geography (ex: global vs. country specific), markets (ex: accross various industries or sector specific) and firm size (ex: large capitalization companies or small capitalization firms). The portfolio is structured and maintained according to the fund’s prospectus, which outlines the fund’s main investment strategies and risk guidelines. An advantage of mutual funds over other investment vehicles is that they give clients with less investable capital access to professionally managed and diversified portfolios.

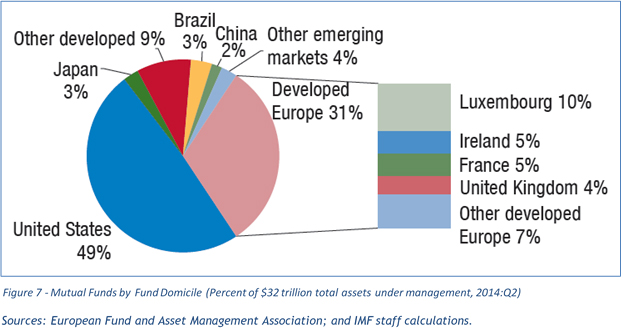

The mutual fund segment is dominated by U.S and European Funds according to the April 2015 IMF report mentioned earlier.

Mutual Funds charge a management expense fee often referred to MER (management expense ratio). The MER is used to cover portfolio management fees as well as various transaction and marketing fees incurred by the portfolio managers in the process of managing the mutual fund.

The MER is computed by dividing the total annual operating expenses of the fund by the average net asset value of the fund. The MER is deducted from the fund’s return.

Here is an example of some of the fees covered by a fund’s MER:

- An account fee is imposed on investors in connection to the maintenance of their accounts, similar to the account-related fees that are charged by banks for savings or checking accounts.

- Exchange fees are paid by the investors in order to transfer from one fund to another within the same fund group.

- Sales Loads are fees are paid by investors to compensate brokers for selling the shares of the fund. This may sometimes be called brokerage fees.

- Distribution Fees are fees paid by the fund out of fund assets to cover distribution expenses and sometimes shareholder service expenses (distribution of prospectuses, various forms and reports to investors)

- The description of the purchase and redemption fees were discussed earlier.

Due to competitive pressures in the industry, mutual fund fees have been declining over the last 15 years. See graph below.

Hedge Funds

Hedge funds are considered alternative investments because they are able to use more leverage (ex: borrowing) as well as short selling (selling a stock now and ideally buying it back for a lower price in the future). In addition, hedge funds are able to take advantage of a wider selection of derivates such as options and futures as well as commodities. Hedge funds aim to generate high returns in any market condition.

Hedge Funds do not need to disclose as much information about their investment strategies as mutual funds do. In addition, being classified as alternative investments, hedge funds are not subject to as much regulatory oversight as mutual funds. Finally, investments in hedge funds are typically locked in for a specific minimum duration.

Typically investors cannot quickly liquidate their investments in a hedge fund. Since hedge funds tend to have a different risk characteristics compared to traditional investments they are only offered to qualified or accredited investors (investors with sufficient knowledge about how capital markets operate or investors with significant net worth).

Hedge funds typically charge two sets of fees:

Assets under management fees are typically set at 2% of the assets that the client invests with the hedge fund manager.

To avoid unnecessary risk-taking by the hedge fund manager in order to potentially generate high returns, most hedge funds have High Watermarks structures in place. In case when the hedge fund manager looses money, High Watermarks prevent the hedge fund manager to collect performance fees until the returns of the fund surpass once more the previously highest attainable return.

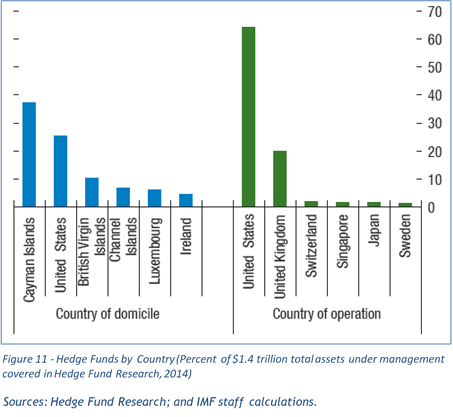

The graph below shows the difference between the countries where most hedge funds are domiciled and the countries where most hedge funds actually operate.

Despite high fees typically associated with hedge funds, many institutional investors have negotiated their fees with their managers. According to a survey done by JP Morgan in 2013, “55% of respondents negotiated the management fee while 34% negotiated the performance fee in 2013, compared to 46% and 29%, respectively, in 2012”. Figure 12 shows the average management fees paid to hedge fund managers in 2012 and 2013.

Exchange Traded Funds

Similarly to traditional mutual funds, Exchange Traded Funds (ETF) enable investors to have access to a basket of securities at a lower price than if these securities needs to be purchased independently. ETFs can be viewed like mutual funds that are traded on the public stock exchanges. Most ETFs are structured to mimic a specific index but at lower management fee compared to traditional mutual funds. Most index replicating ETFs do not have a portfolio managers who makes the investment decisions such as in a mutual funds. Instead, the allocation of an ETFs is predominately done by computer algorithms. Since ETFs require less management oversight, they often have smaller management fees compared to traditional mutual funds.

| Fund Type |

Average Total Operating Expenses |

||

| Mutual Funds |

ETFs |

||

| US Large-Cap Stock |

1.31% |

0.47% |

|

| US Mid-Cap Stock |

1.45% |

0.56% |

|

| US Small-Cap Stock |

1.53% |

0.52% |

|

| International Stock |

1.57% |

0.56% |

|

| Taxable Bond |

1.07% |

0.30% |

|

| Municipal Bond |

1.06% |

0.23% |

|

Compared to mutual funds, ETFs have lower operating expenses and no load fees. FINRA’s comparison of expenses is posted on its website.

Another important difference between EFTs and traditional mutual funds is inter-day trading. Traditional mutuals funds can only be purchased or sold at the end of a trading day. Every investor who decides to either purchase or sell units of a mutual fund will receive the same price that will be set once the closing prices of the individual securities that are part of the mutual fund will be know.

Since an ETF actually trades on the stock exchange, it can be purchased or sold during a given trading day multiple times over. The market price of an ETF is know at any given time during the trading day.

Due to the underlying structure of ETFs, they are considered to be more tax advantageous than traditional mutual funds.

Private Equity Fund

Private equity funds are also considered as alternative investments. Private equity funds can specialize in a variety of investment strategies. For example, a private equity fund can take a public company private. During the process of corporate re-organization, the management of the private equity fund will make the business more efficient and either bring the company back to the public market or divide the company’s assets into separate entities and sell these entities to different buyers.

Similarly to hedge funds, private equity funds tend to have a longer investment time horizon and have a risk/return profile that is different from traditional mutual funds. For these reasons, private equity funds are also tailored to high net worth individuals and accredited investors.

Similarly to hedge funds, private equity funds tend to have a management fee that is related to the size of the assets under management as well as performance fees that are related to the overall performance of the fund over a given time period.

Resources and further readings

J.P. Morgan. (2014). Institutional Investor Survey – 2014.

Anspach, D. (2015, July 24). 6 Investment Fees To Ask About Before You Invest. Retrieved from About.com: http://moneyover55.about.com/od/howtoinvest/a/feesexpenses.htm

Deuskar, P., Wang, Z., Wu, Y., & Nguyen, Q. (2011). The Dynamics of Hedge Fund Fees. Illinois.

Feng, S. (2011). Three Essays on Hedge Fund Fee Structure, Return Smoothing and Gross Performance. Massachusetts: University of Massachusetts.

FIL Investment Management (Hong Kong) Limited. (2015, July 24). What fees are charged. Retrieved from Fidelity Worldwide Investment: https://www.fidelity.com.hk/investor/en/learn-about-investing/learn-about-funds/what-fees-are-charged.page

Financial Industry Regulatory Authority, Inc. (2015, July 25). Exchange-Traded Funds. Retrieved from FINRA Web site: http://www.finra.org/investors/exchange-traded-funds

Financial Services Users Group of European Commission. (2014). ASSET MANAGEMENT: FSUG POSITION PAPER. Brussels: European Commission.

International Monetary Fund. (2015). Chapter 3: The Asset Management Industry and Financial Stability. In Global Financial Stability Report: Navigating Monetary Policy Challenges and Managing Risks (pp. 93-135). April.

Mutual Fund Fees and Expenses. (2013, January 15). Retrieved from U.S. Securities and Exchange Commission: http://www.sec.gov/answers/mffees.htm

{kind=link}