Canadian IPO – Primer on the Canadian Private to Public Market

Canadian IPO – Canadian Private to Public Market

An initial public offering (IPO) is the most common procedure for a private company to become public. In the IPO process, the company issues shares of stocks to the public and lists these securities on a stock exchange.

Companies go public primarily to acquire more capital from outside the company for the expansion or improvement of its business operations. Going public also enhances the credibility of the company with the public, as well as its corporate image. As a result, other financing avenues for the company can be facilitated.

For investors, investing in a public company has its benefits as well. When the stocks are listed on an exchange, investors can easily buy or sell their shares in the secondary market.

However, going public does not only have benefits, there are also costs for the company. These includes not only the fees charged by underwriters and other parties to the IPO but also costs and other continuing obligations after the completion of the IPO. One important obligation of the company to the public is to disclose material information through the exchange including its financial results, management and director performance or changes, executive compensation, corporate governance practices, and insider trading information. These obligations opens the company to public scrutiny and limits its transaction freedom.

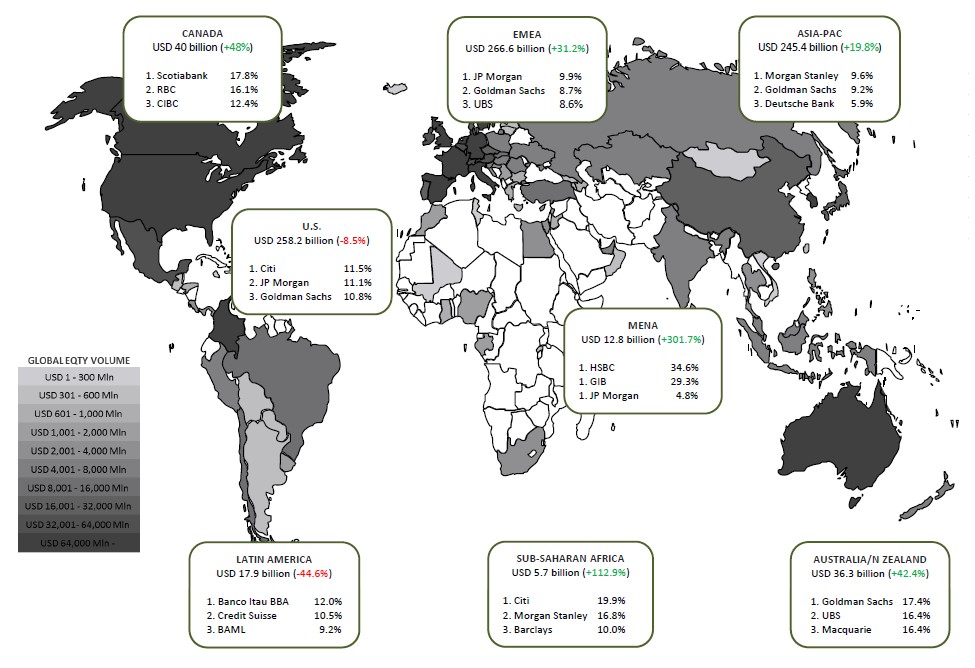

Despite the costs, 2014 was a strong year for initial public offerings globally. Refer to image below for the snapshot of Equity, Equity Linked, and Rights offerings globally as presented by Bloomberg in its 2014 Edition of Global Equity Capital Markets League Tables.

In Canada, the total of IPOs across the country totaled USD 40 billion for 2014. According to KPMG, Oil and Gas was the most active sector earlier in 2014 but its activity dropped as oil prices retreated. Other new issuers were from the following sectors: mining, financial services, technology, manufacturing, and healthcare sectors.

Top 10 IPOs of Companies in Canada in 2014

| Company Name | Year EndMarket Value (USD) |

Sector | |

| 1 | PrairieSky Royalty Ltd. | 3,715,001,359.02 | Oil & Gas |

| 2 | Seven Generations Energy Ltd. | 3,474,590,473.95 | Oil & Gas |

| 3 | Callidus Capital Corporation | 692,762,355.69 | Financial Services |

| 4 | Northern Blizzard Resources Inc. | 660,914,178.59 | Oil & Gas |

| 5 | Kinaxis Inc. | 356,006,299.19 | Technology |

| 6 | Lumenpulse Inc. | 310,723,866.67 | Clean Technology |

| 7 | Journey Energy Inc. | 144,846,767.97 | Oil & Gas |

| 8 | NYX Gaming Group Limited | 103,047,396.34 | Technology |

| 9 | DataWind Inc. | 61,658,576.71 | Technology |

| 10 | Rockefeller Hughes Corporation | 18,498,035.33 | Oil & Gas |

| Average | 953,804,930.95 |

Comparison of Historical Largest IPOs in Canada and in USA

| USA | Canada | |||

| Company | IPO Value (in USD Billions) |

Company | IPO Value (in USD Billions) |

|

| 1 | Alibaba Holdings Group | 21.80 | MEG Energy Corp | 7.02 |

| 2 | The Agricultural Bank of China | 19.20 | Athabasca Oil Sands Corp | 4.90 |

| 3 | Industrial and Commercial Bank of China | 19.10 | PrairieSky Royalty Ltd. | 3.72 |

| 4 | NTT Mobile Communications Network | 18.40 | Seven Generations Energy Ltd. | 3.47 |

| 5 | Visa | 17.90 | Genworth MI Canada Inc. | 2.58 |

| 6 | AIA | 17.82 | Tourmaline Oil Corp. | 2.41 |

| 7 | Enel SpA | 16.58 | Tahoe Resources Inc | 1.68 |

| 8 | 16.01 | Hudson’s Bay Company | 1.63 | |

| 9 | GM | 15.80 | Gibson Energy Inc. | 1.50 |

| 10 | Nippon Tel | 15.30 | Dollarama Inc | 1.32 |

| Average IPO Size of the Top 10 Largest | 17.79 | 3.02 | ||

The Toronto Stock Exchange (TSX), is becoming an increasingly appealing exchange for foreign companies, having more than 300 foreign companies listed from the United States, China, Israel, United Kingdom, and more.

Canadian IPO process

The IPO process is a tedious process for a company to undergo. There are a lot of rules and regulations that the company needs to comply with and in Canada, securities regulation is a provincial matter. Each province has its own securities legislation but the requirements are generally consistent across the country. In an effort to coordinate the regulation of the markets, the provinces work together through the Canadian Securities Administrators (CSA). The CSA has been developing uniform rules and guidelines, coordinating approval processes, developing national electronic filing systems and coordinating compliance and enforcement activities. CSA’s online system, System for Electronic Document Analysis and Retrieval (SEDAR), whereby prospectuses and continuous disclosure documents can be filed with the various securities commissions and viewed by the public, provides access to all Canadian public company filings under applicable securities laws on its website (www.sedar.com). The CSA also has an online system for insider reporting filings, the System for Electronic Disclosure by Insiders (SEDI).

Now, let us discuss the IPO process.

1. Initiation

Before the launch of the IPO, the company must first assess its expected valuation. Valuation involves assessment of the company’s equity value to determine the potential market value of the securities to be offered. Other important items and processes that must be considered include the type of the securities to offer, share structure, the requirement for audited financial statements, a due diligence review, and third party consents.

Should a company decide to go public, they will have to go through underwriting firms. These are usually the investment banking division of banks. The lead underwriter assumes the responsibility of managing the whole IPO process. Their responsibilities include:

- Drafting and filing the prospectus

- Marketing the stocks to prospective investors

- Distributing the stocks to investors and transmitting the cash to the issuing company

- Determining the initial price of the stocks

2. Preparing the issue

The preliminary prospectus is the document that contains full, true and plain disclosure of all material facts related to the securities to be offered. It contains the company’s financial statements and information concerning the following:

- business carried on by the company, including how it markets and sells its products and services,

- its customers,

- its intellectual property rights,

- its employees and its properties,

- the industry and markets in which the company operates and any trends affecting the company;

- the officers and directors of the company and their background and skills;

- the principal security holders of the company and the number and type of securities each principal security holder holds;

- any material transactions of the company in the previous three years in which management and other persons related to the company had an interest;

- any particular risk factors associated with the business or an investment in the company’s securities;

- the issuances of the company’s securities in the previous year and the prices at which the securities were issued; and

- how the company intends to use the proceeds of the IPO.

Once the preliminary prospectus has been drafted, the next step is to file this with the Securities and Exchange Commission (SEC) for the registration of the security. But because each province and territory in Canada has its own “SEC”, the issuer must file a prospectus and other requirements for the registration of the securities in each jurisdiction in which it wishes to issue shares. With National Policy 11-202, Process for Prospectus Reviews in Multiple Jurisdictions, the issuer can access markets in several jurisdictions by dealing with only one regulatory authority through a “passport system”, which acts as a passport for the issuer for other jurisdictions. All markets across Canada participates in this system except Ontario. The issuer must also submit a separate set of requirement to the Ontario Securities Commission should it wish to access the Ontario market.

The regulatory authority shall review the preliminary prospectus and issue comments and changes that must be done by the issuer. Additional requirements that must be submitted to the regulator includes: personal information forms from each director and executive officer of the company, fund manager, and promoter; and material contracts and other documents.

After the clearance process, the final prospectus will be filed. The final prospectus must then contain the total number of shares and price of the securities.

3. Pricing

A roadshow, a two to four-week marketing effort, is done by the underwriters to determine the interest in the new issue. Investor interest, in terms of the price and volume at which investors are willing to buy, is then recorded in an order book.

Based on the investor interest, the underwriters will determine the pricing of the shares and the volume that will be issued. The initial terms will be adjusted accordingly according to the investor demand on the new shares.

4. Distribution

Individual investors will have difficulties in buying shares in an IPO because the underwriters usually prioritize institutional investors. This is because institutional investors are able to purchase large blocks and can better handle risks.

Upon finalization of the number of shares being issued, the shares will be distributed to the investors. Then, payments will be collected and remitted to the issuer.

5. Listing

The securities must also be listed on a stock exchange, which provides companies access to public equity and gives existing and new investors a platform for the liquidity of the securities. A company seeking to list its securities must file a listing application and other supporting data to the exchange. Specified minimum financial, distribution, and other standards must be met for the securities to be listed. Upon approval, a listing agreement with the exchange will be entered into by the company. This agreement specifies the continuing obligations of the company including disclosure requirements and other reporting obligations.

On the TSX, companies categorized in the following sectors: Industrial (General), Mining, or Oil and Gas. Once listed, the company must have at least one million freely tradable shares with an aggregate market value of at least CDN$ 4 million held by at least 300 public shareholders, each holding at least one “board lot”. Other than this, the company must also demonstrate that it has satisfactory management expertise and experience relating to the company’s business and industry, including its public company experience. The company’s management team must have at least two independent directors, a chief executive officer, a chief financial officer, and a corporate secretary.

The TSX designates the company as either an exempt or non-exempt issuer. This pertains to the need for a sponsorship by a Canadian registered dealer or affiliation with an established issuer on the TSX can play a significant role in determining the suitability of a company for listing on the TSX. In the case of a mining applicant company, the company must also prove reserves capable of providing a mine life of at least three years.

The TSX Ventures Exchange (TSX-V) is the exchange where emerging companies, with a focus on the resource sector, are listed. Its listing requirements are aimed more toward management experience than toward a company’s products and services. TSX-V categorizes companies in two tiers on the basis of historical financial performance, stage of business development, and financial resources.

- Tier 1: Companies with greater financial resources; has more minimum listing requirements and tier maintenance requirements; must have at least one million freely tradable shares with an aggregate market value of at least CDN$ 1 million, held by at least 200 public shareholders, each holding at least one board lot.

- Tier 2: Early-stage companies in all industry sectors; must have at least 500,000 freely tradable shares with an aggregate market value of at least CDN$ 500,000, held by at least 200 public shareholders, each holding at least one board lot.

The TSX-V contains more tier 2 issuers, any of which can reach tier 1 status upon meeting the tier 1 minimum listing requirements.

Issuers listed on the TSX-V may also graduate to TSX upon completion of TSX’s listing requirements. In 2014, 22 companies graduated from TSX-V to TSX.

The completion of the distribution and listing of the notes will mark the end of the IPO process for the issuer. The company may choose to do a secondary issue should it need more capital.

Public Company

Upon closing of the IPO, the company starts its life as a public company. Certain processes will be changed to consider the public investors in every major decisions that the company must take. In addition, the company must continuously follow the regulations for public companies particularly in the areas of governance, disclosure requirements, and other issues.

The continuing disclosures requirements, which aims to ensure that disclosure similar to that contained in the prospectus is available to securities markets at all times, include the following:

- Annual Information Form

- Financial statements

- Management’s discussion and analysis

- Information circular

- Disclosure of material changes

- Business acquisition report

- Certifications

Relevant Market Data

A. TMX Group Equity Financing Statistics – May 2015

Tables from TMX Website

Toronto Stock Exchange

As of end of May 2015, the total number of issues listed on the TSX is 2,241 by 1,518 issuers, totaling CDN$ 2.6 trillion.

| May 2015 | April 2015 | May 2014 | |

| Issuers Listed | 1,518 | 1,510 | 1,498 |

| New Issuers Listed | 18 | 8 | 7 |

| IPOs | 15 | 8 | 4 |

| Graduates from the TSV-X | 1 | 0 | 3 |

| Issues Listed | 2,241 | 2,237 | 2,172 |

| IPO Financings Raised | CDN$ 779,993,605 | CDN$ 404,945,508 | CDN$ 1,686,150,000 |

| Secondary Financings Raised | CDN$ 1,354,341,272 | CDN$ 4,203,080,723 | CDN$ 1,816,038,521 |

| Supplemental Financings Raised | CDN$ 3,153,404,619 | CDN$ 2,749,620,278 | CDN$ 2,196,770,000 |

| Total Financings Raised | CDN$ 5,287,739,496 | CDN$ 7,357,646,509 | CDN$ 5,698,958,521 |

| Total Number of Financings | 72 | 59 | 52 |

| Market Cap Listed Issues | CDN$ 2,604,677,733,181 | CDN$ 2,638,388,002,427 | CDN$ 2,496,405,766,009 |

Year-to-Date Statistics

| 2015 | 2014 | % change | |

| New Issuers Listed | 54 | 45 | +20.0 |

| IPOs | 49 | 31 | +58.1 |

| Graduates from the TSV-X | 3 | 10 | -70.0 |

| IPO Financings Raised | CDN$ 2,357,326,839 | CDN$ 2,960,770,000 | -20.4 |

| Secondary Financings Raised | CDN$ 16,322,887,073 | CDN$ 7,074,767,781 | +130.7 |

| Supplemental Financings Raised | CDN$ 10,584,821,077 | CDN$ 12,625,140,828 | -16.2 |

| Total Financings Raised | CDN$ 29,265,034,989 | CDN$ 22,660,678,609 | +29.1 |

| Total Number of Financings | 284 | 263 | +8.0 |

| Market Cap Listed Issues | CDN$ 2,604,677,733,181 | CDN$ 2,496,405,766,009 | +4.3 |

TSX Venture Exchange

As of end of May 2015, the total number of issues listed on the TSX-V is 2,343 by 2,280 issuers, totaling CDN$ 28.4 billion.

| May 2015 | April 2015 | May 2014 | |

| Issuers Listed | 2,280 | 2,302 | 2,415 |

| New Issuers Listed | 2 | 5 | 7 |

| IPOs | 0 | 4 | 2 |

| Graduates to TSX | 1 | 0 | 3 |

| Issues Listed | 2,343 | 2,369 | 2,480 |

| IPO Financings Raised | CDN$ 0 | CDN$ 23,373,916 | CDN$ 700,000 |

| Secondary Financings Raised | CDN$ 257,745,715 | CDN$ 0 | CDN$ 160,532,212 |

| Supplemental Financings Raised | CDN$ 158,434,568 | CDN$ 139,348,761 | CDN$ 238,363,866 |

| Total Financings Raised | CDN$ 416,180,283 | CDN$ 162,722,677 | CDN$ 399,596,078 |

| Total Number of Financings | 109 | 98 | 138 |

| Market Cap Listed Issues | CDN$ 28,397,780,379 | CDN$ 28,315,077,803 | CDN$ 34,428,905,753 |

Year-to-Date Statistics

| 2015 | 2014 | % change | |

| New Issuers Listed | 20 | 27 | -25.9 |

| IPOs | 11 | 7 | +57.1 |

| Graduates to TSX | 3 | 10 | -70.0 |

| IPO Financings Raised | CDN$ 40,925,616 | CDN$ 5,992,806 | +582.9 |

| Secondary Financings Raised | CDN$ 363,537,539 | CDN$ 588,596,232 | -38.2 |

| Supplemental Financings Raised | CDN$ 870,472,226 | CDN$ 1,587,117,821 | -45.2 |

| Total Financings Raised | CDN$ 1,274,935,381 | CDN$ 2,181,706,859 | -41.6 |

| Total Number of Financings | 551 | 748 | -26.3 |

| Market Cap Listed Issues | CDN$ 28,397,780,379 | CDN$ 34,428,905,753 | -17.5 |

B. 2015 vs. 2014 YTD IPO Breakdown by Asset Class (As of End of May)

Data from TMX Website

| TSX-V | TSX | |||||

| 2015 YTD | 2014 YTD | Change | 2015 YTD | 2014 YTD | Change | |

| IPOs (ex CPCs/ETFs/CEFs/SPACs) | 4 | 1 | +300% | 4 | 3 | +33% |

| CPC/SPAC IPOs | 7 | 6 | +17% | 2 | 0 | +100% |

| ETF & Closed-End Fund IPOs | 43 | 28 | +54% | |||

| Qualifying Transactions (QTs) | 12 | 20 | -40% | |||

| TSXV RTOs | 4 | 7 | -43% | |||

| NEX RTOs | 0 | 1 | -100% | |||

| Grad | 3 | 10 | -70% | |||

| Other | 9 | 20 | -55% | 2 | 4 | -50% |

C. Consolidated Issuers Data by Geography – April 2015

Data from TMX Website

Toronto Stock Exchange

TSX Venture Exchange

D. Canadian Issuers Listed on TSX and TSX-V – April 2015

Data from TMX Website

Toronto Stock Exchange

As of end of April 2015, 91.66% of all issuers listed on the TSX are issuers from Canada.

| All Issuers | Canadian | Canadian as % of All Issuers | |

| Number of Issuers | 1,510 | 1384 | 91.66 |

| QMV (C$ Billions) | 2,638.5 | 2,486.6 | 94.24 |

TSX Venture Exchange

As of end of April 2015, 93.12% of all issuers listed on the TSX-V are issuers from Canada.

| All Issuers | Canadian | Canadian as % of All Issuers | |

| Number of Issuers | 1,945 | 1,811 | 93.12 |

| QMV (C$ Billions) | 28.0 | 25.0 | 89.29 |

E. USA Issuers Listed on TSX and TSX-V – April 2015

Data from TMX Website

Toronto Stock Exchange

As of end of April 2015, 3.77% of all issuers listed on the TSX are issuers from the USA.

| All Issuers | USA | USA as % of All Issuers | |

| Number of Issuers | 1,510 | 57 | 3.77 |

| QMV (C$ Billions) | 2,638.5 | 100.3 | 3.80 |

TSX Venture Exchange

As of end of April 2015, 3.90% of all issuers listed on the TSX-V are issuers from the USA.

| All Issuers | USA | USA as % of All Issuers | |

| Number of Issuers | 1,945 | 76 | 3.90 |

| QMV (C$ Billions) | 28.0 | 2.1 | 7.50 |

F. International Issuers Listed on TSX and TSX-V – April 2015

Data from TMX Website

Toronto Stock Exchange

As of end of April 2015, 4.57% of all issuers listed on the TSX are issuers from outside Canada or USA.

| All Issuers | International | International as % of All Issuers | |

| Number of Issuers | 1,510 | 69 | 4.57 |

| QMV (C$ Billions) | 2,638.5 | 51.6 | 1.96 |

TSX Venture Exchange

As of end of April 2015, 2.98% of all issuers listed on the TSX-V are issuers from outside Canada or USA.

| All Issuers | International | International as % of All Issuers | |

| Number of Issuers | 1,945 | 58 | 2.98 |

| QMV (C$ Billions) | 28.0 | 0.9 | 3.21 |

Relevant Studies

Cécile Carpentier and Jean-Marc Suret conducted a study in 2007, The Survival and Success of Penny Stock IPOs: Canadian Evidence. The study analyzed the survival and success of Canadian IPOs based on an original sample of 2,373 issues, free of selection or survival bias, from 1986 to 2003. They concluded that, “Canadian IPO market differs sharply from markets in the rest of the world, due to very low initial listing standards. The large majority of the new issues are micro or penny stock IPOs, and 45% of the issuers report no revenues. Only 10% of issuers would meet the level 2 standards of NASDAQ. Contrary to the situation observed in the U.S., the new listing of small companies without earnings is not a recent phenomenon; it can be observed in Canada in the ‘80s.” The results of their study has several implications for regulators and policy makers including that “allowing firms to enter the stock market at a pre-revenue stage is a perilous strategy”.

Another research study on the IPO market in Canada has been conducted by Bryce C. Tingle, J. Ari Pandes, and Michael J. Robinson (2012), published in the Canadian Business Law Journal, to determine why the effect of the 2008 financial crisis in the Canadian IPO market is not as evident as compared to the US and other markets in the terms of new IPOs. According to the study, the main reason for this is that the companies were going public in markets outside of their home jurisdictions in an attempt to overcome the adverse effects of poor local laws and regulation. The regulations in the Canadian markets seemed to be more conducive to IPOs. Smaller companies also find it easier to do an IPO in Canada due to the existence of ventures stock exchanges that facilitates listing of smaller companies.

On another topic, Jean Bédard, Daniel Coulombe, and Lucie Courteau (2008) examined the role of audit committees in the Initial Public Offering (IPO) process in a setting where audit committee (AC) best practices are known but their adoption is voluntary. They analyzed archival data from a sample of 246 IPOs issued in the Canadian province of Québec over the period 1982 to 2002 and found that “the mere creation of an audit committee at the time of the IPO has no effect on underpricing unless its members are independent and have expertise in financial matters, in which case it decreases significantly the level of underpricing of the IPO. However, we find no significant association between these two governance attributes and the accuracy of forecasts included in prospectus.” Their results stressed the importance of the presence of qualified members on the AC, i.e. members with sufficient knowledge of accounting and finance, which is consistent with the recent legislations in several countries.

Resources and further readings

Bloomberg Finance L.P. (2014). Global Equity Capital Markets League Tables.

Carpentier, C., & Suret, J.-M. (2007). The Survival and Success of Penny Stock IPOs: Canadian Evidence. Québec Canada.

KPMG. (2015). KPMG: IPO Services. Retrieved from KPMG Website: https://www.kpmg.com/Ca/en/topics/IPO-Services/Documents/Canadas-equtiy-capital-markets-2015-Salma-Salman.pdf

KPMG LLP. (2015, June 3). KPMG: A Guide to Going Public. Retrieved from KPMG Website: http://www.kpmg.com/ca/en/issuesandinsights/articlespublications/pages/a-guide-to-going-public.aspx

MORRIS, V. B., & GOLDSTEIN, S. Z. (2010). Life Cycle of a Security. New York, New York, USA.

Tingle, B. C., Pandes, J., & Robinson, M. J. (2012). THE IPO MARKET IN CANADA: WHAT A COMPARISON WITH THE UNITED STATES TELLS US ABOUT A GLOBAL PROBLEM. Canadian Business Law Journal, 321-367.

Torys LLP. (2011, March 11). Torys LLP: Insights. Retrieved from Torys LLP Website: http://www.torys.com/insights/publications/2011/03/initial-public-offerings-in-canada

{kind=link}